Siemens operates at a scale few companies can match: It competes across an exceptionally wide set of industries, from industrial automation and factory digitalization to medical imaging, smart infrastructure, energy systems, and rail mobility.

What makes Siemens even more unique is the breadth of its digital ecosystem. Its software platforms, such as Teamcenter, NX, Simcenter, and the MindSphere IoT cloud, are used by more than 100,000 manufacturers worldwide, and Siemens holds over 41,700 patents across automation, energy, industrial software, and healthcare engineering. [1]

Below, we explore all major Siemens competitors across each of its core business units. From automation to healthcare, rail systems to digital software, we break down the companies that are shaping the race for industrial leadership.

Did you know?The global industrial automation and control systems market size is projected to surpass $378.5 billion by 2030, growing at a 10.8% annual rate. This strong growth is mainly driven by manufacturers wanting higher efficiency, better accuracy, and improved safety in their operations. [2]

Table of Contents

15. Omron Corporation

Founded in 1933Headquarters: Kyoto, Japan

Revenue: $5.3 billion+

Competitive Edge: Advanced machine vision & robotics

Omron Corporation is a Japanese electronics and automation company focused on control systems, advanced sensors, machine vision, robotics, and medical devices.

It produces photoelectric sensors, proximity switches, safety light curtains, servo drives, and machine controllers. These products are used in thousands of facilities across industries such as electronics, automotive, packaging, pharmaceuticals, food processing, and logistics.

In PLC (programmable logic controller) controllers, Omron’s Sysmac series competes directly with Siemens’ SIMATIC PLC family. In machine vision and robotics, Omron competes with Siemens’ automation ecosystem through its advanced vision systems and integrated robotics capabilities.

Omron’s mobility robots are used in factories, labs, hospitals, and distribution centers to automate material handling, improving efficiency and reducing human risk.

The company also produces medical devices, such as blood pressure monitors, thermometers, nebulizers, and body composition analyzers. In fact, they sell tens of millions of blood pressure monitors globally and hold one of the highest global market shares in personal cardiovascular monitoring devices. [3]

14. Yokogawa Electric

Founded in 1915Headquarters: Tokyo, Japan

Revenue: $3.7 billion+

Core rivalry: Process automation

Competitive Edge: Strong chemical and oil & gas specialization

Yokogawa is one of Siemens’ strongest competitors in process automation, industrial instrumentation, and advanced control systems, although the two companies differ in geographic influence and product breadth.

Siemens has a broader automation and software portfolio, while Yokogawa is highly specialized in process industries with unmatched reliability and niche excellence.

Its Distributed Control System (DCS), called CENTUM, is one of the longest continuously evolving DCS platforms. It is widely used in complex process plants where uptime, reliability, and safety are critical, and supports thousands of refineries, LNG plants, chemical facilities, and power stations worldwide.

The company has also built a strong reputation in industrial measurement and instrumentation, offering world-class sensors, analyzers, and precision devices, including flow meters, pressure transmitters, gas analyzers, chromatographs, and level gauges.

Plus, Yokogawa has expanded into industrial IoT, cloud data platforms, and predictive analytics. It invests over $200 million annually in R&D, focusing on industrial digitization, AI-assisted diagnostics, autonomous process operations, and energy transition technologies such as hydrogen production monitoring and carbon capture system automation. [4]

On the ESG side, Yokogawa was recognised with a double “A” score for transparency on climate change and water security in 2025 for the second consecutive year. [5]

13. Danfoss

Danfoss headquarters Denmark

Danfoss headquarters Denmark

Headquarters: Nordborg, Denmark

Revenue: $11 billion+

Core rivalry: Motor drives (VFDs), Industrial automation

Competitive Edge: Focus on energy efficiency and sustainability

Danfoss is a respected industrial engineering company that plays a central role in climate control, energy-efficient solutions, and hydraulic systems for mobile machinery. It aims to increase machine productivity, reduce emissions, lower energy consumption, and enable electrification.

It operates 100+ factories globally and employs about 39,000 people.

The company has built a world-class reputation in power electronics, especially through its Danfoss Drives division, which produces variable frequency drives (VFDs). These drives are used extensively in HVAC systems, water treatment plants, industrial machinery, marine applications, conveyors, and energy optimization systems.

In energy efficiency and climate technology, Danfoss competes with Siemens in solutions supporting decarbonization, industrial energy optimization, and sustainable cooling/heating. Danfoss is particularly strong in refrigeration and heat pump technologies, whereas Siemens focuses more on grid-level energy systems and smart buildings.

The company also manufactures hydraulic pumps, motors, steering units, valves, and electronic controls used in construction machinery, agricultural equipment, and industrial machinery. These systems are engineered for high reliability in demanding environments, making Danfoss a preferred partner for global OEMs in heavy equipment industries. [6]

12. CRRC Corporation

Headquarters: Beijing, China

Revenue: $34 billion+

Core rivalry: Rail systems, locomotives, metro systems

Competitive Edge: Strong support from National Infrastructure Policy

CRRC Corporation is a Chinese state-owned enterprise and publicly traded company that manufactures and services rail transit equipment, including rolling stock, locomotives, metro cars, and freight wagons.

It manufactures thousands of railcars each year, making it the world’s largest rolling stock producer. Its high-speed train platforms (often operating at speeds of 300-380 km/h) form the backbone of China’s extensive high-speed railway network, the largest in the world.

According to Forbes, the company earns about $34 billion in revenue, holds roughly $70.6 billion in assets, and employs around 152,000 people.

Compared to Siemens, which dominates technologically advanced and digitally integrated rail systems (particularly in Europe and high-income regions), CRRC dominates global rolling stock production and large-scale railway projects (especially in developing markets).

In the locomotive and freight rail sectors, CRRC is the largest supplier worldwide, producing diesel and electric locomotives for both domestic and international markets. Siemens Mobility also has a strong locomotive portfolio (such as Vectron), but CRRC’s scale gives it a competitive advantage in emerging economies.

11. Bosch Rexroth

Headquarters: Lohr am Main, Germany

Revenue: $8 billion+

Core rivalry: Industrial hydraulics, motion control

Competitive Edge: Modular product architecture and engineering efficiency

Bosch Rexroth focuses on hydraulics, factory automation, motion control, drive systems, and industrial robotics integration. As a wholly owned subsidiary of the global Bosch Group, it benefits from deep engineering expertise and a massive industrial footprint.

The company produces some of the world’s most durable and high-performance hydraulic pumps, motors, valves, cylinders, and manifolds used in heavy machinery, construction equipment, material handling systems, and industrial production lines. It also supplies axial piston pumps, planetary drives, hydraulic power units, and load-sensing systems.

Rexroth’s automation portfolio includes electric drives, linear motion systems, servo motors, controllers, SCARA robots, and precision positioning equipment. Its IndraDrive and IndraControl platforms are widely used in industrial machinery, packaging systems, woodworking, printing, and semiconductor production.

These platforms directly compete with Siemens’ SINAMICS drives and SIMOTION controllers.

Rexroth is also one of the pioneers of the factory-of-the-future concept. It integrates IoT, edge computing, AI-enabled diagnostics, smart actuators, and digital twins through its open automation platform, ctrlX AUTOMATION.

This platform allows customers to use app-based automation architectures, open-source frameworks, and cloud-native control systems, making Rexroth a key contributor to next-generation digital manufacturing.

10. Emerson Electric

Founded in 1890Headquarters: Missouri, US

Revenue: $18 billion+

Core rivalry: Automation control valves, process automation

Competitive Edge: Expertise in measurement & control

Emerson Electric develops process automation systems, control valves, measurement devices, industrial IoT platforms, and optimization software.

The company focuses on three levers in its value creation framework: organic growth, portfolio management (including divestitures and acquisitions), and operational excellence.

Its flagship DeltaV Distributed Control System (DCS) and Ovation control platform are installed across power plants, refineries, chemical facilities, LNG terminals, water treatment systems, and large-scale manufacturing facilities. These DCS systems often operate continuously for decades, creating long-term service relationships and recurring revenue streams.

Emerson also manufactures valves, actuators, regulators, sensors, transmitters, gas analyzers, and compressors. Its valve and instrumentation products are sold under well-known brands such as Fisher, Rosemount, Bettis, and Micro Motion. These brands hold strong market positions, especially in pressure, flow, temperature, and level measurement.

In FY 2025, the company generated nearly $18.02 billion in net sales, a 3% year-over-year increase. Its financial report highlighted strong backlog growth and momentum in large projects, with the backlog reaching $7.4 billion, up 3% from the previous year. [7]

9. Alstom

Headquarters: Paris, France

Revenue: $20 billion+

Core rivalry: Rail mobility, signalling, and rolling stock

Competitive Edge: Strong global backlog and forward visibility

Alstom is known for its expertise in high-speed trains, metros, trams, locomotives, signaling systems, and railway infrastructure services. With annual revenue of $20 billion and a workforce of around 86,000 people, it is the largest dedicated rail manufacturer in Europe and one of the top three rail mobility companies worldwide. [8]

Alstom’s most iconic achievement is the creation of the TGV high-speed train, one of the fastest and most successful high-speed rail platforms ever developed. The company also manufactures the AGV and Avelia high-speed train families.

Besides high-speed systems, Alstom has delivered tens of thousands of metros, commuter trains, trams, and light-rail vehicles, making it one of the largest rolling stock suppliers in the world.

Plus, the company develops rail signaling technologies, where its systems control thousands of kilometers of railway networks around the world. Its signaling portfolio includes advanced ETCS (European Train Control System), CBTC (Communication-Based Train Control), interlockings, train control systems, and digital command centers.

Alstom also generates revenue (15-20%) from its extensive rail infrastructure services, which include maintenance, modernization, spare parts, depot management, predictive analytics, and long-term service agreements.

In FY 2025, Alstom received about €23 billion in new orders. Its order backlog stood at around $110 billion, giving the company strong visibility for future revenue.

8. Hitachi

Founded in 1910Headquarters: Tokyo, Japan

Revenue: $45 billion+

Core rivalry: Rail systems, industrial automation

Competitive Edge: Global reach + Japanese engineering heritage

Hitachi has undergone a massive transformation from a sprawling electronics conglomerate into a streamlined, digital-forward industrial leader. It has doubled down on core businesses like rail transportation, automation systems, energy infrastructure, and digital transformation technologies.

Hitachi Rail, for example, supplies advanced rolling stock, electric trains, metros, signaling technologies, and railway maintenance systems. This makes it a direct competitor to Siemens Mobility in several global rail markets.

While Siemens leads strongly in European high-speed mobility, Hitachi has expanded aggressively in Europe and Asia, winning major high-speed rail and metro contracts. Their competition extends to signaling (ETCS/CBTC), rolling stock, railway electrification, and railway digitalization platforms.

One of Hitachi’s key strategic priorities is its Lumada platform business, which focuses on digital, IoT, and data analytics solutions. Lumada generated over $19 billion in revenue in FY 2025, up about 29% from the previous year, highlighting Hitachi’s strong shift toward digital-first infrastructure.

Another core pillar is its industrial and energy systems division, which produces grid equipment, electrical transformers, industrial motors, pumps, inverters, power electronics, and renewable energy systems.

Through its subsidiary Hitachi Energy , the company has a strong presence in grid modernization, transmission systems, and renewable energy infrastructure. In 2024, Hitachi Energy signed contracts worth over $2 billion with German grid operator Amprion GmbH for high-voltage converter stations, reinforcing its global grid-business strength. [9]

7. Honeywell

Headquarters: Indiana, US

Revenue: $40.6 billion+

Core rivalry: Building automation, aerospace electronics, industrial software

Competitive Edge: Diversified and large portfolio, financially strong

Honeywell competes with Siemens in several strategic markets, particularly in industrial automation, smart infrastructure, energy management, and security and fire safety systems.

In industrial automation, Honeywell’s DCS (Distributed Control Systems) competes closely with Siemens’ PCS 7 and its process automation solutions. It has a strong customer base in oil & gas, refining, chemicals, and heavy process industries.

In building automation, Honeywell’s EBI (Enterprise Buildings Integrator) and its HVAC controls, fire safety systems, and security platforms rival Siemens’ Desigo CC and Smart Infrastructure solutions. Honeywell has quite an edge in large commercial buildings, airports, and critical infrastructure facilities.

Today, more than 10 million commercial buildings utilize Honeywell technologies to improve performance and create safer, more comfortable spaces.

In industrial software, both companies offer IIoT platforms. Honewell Forge, for example, excels in operational performance analytics and industrial cybersecurity.

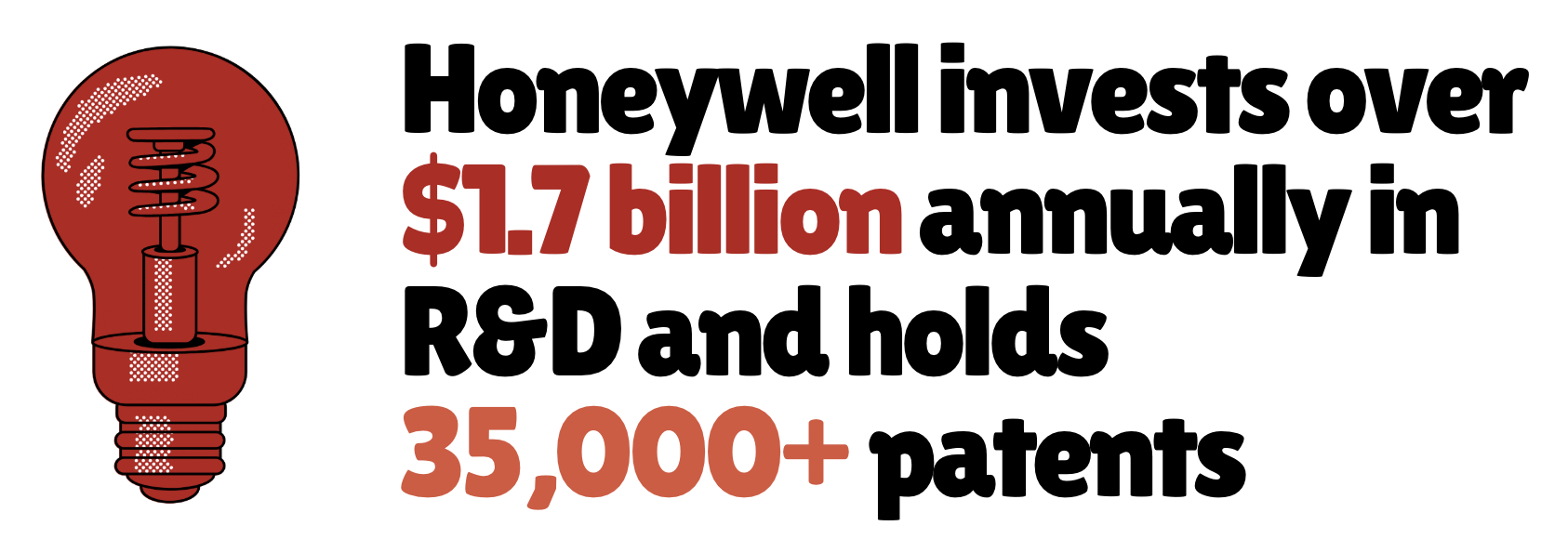

In recent years, Honeywell has deliberately focused on megatrends such as automation, aerospace, and defense. In FY 2025, the company reported $40.67 billion in revenue and $80.9 billion in total assets, reflecting a 10.1% YoY increase (in assets). [10]

6. Mitsubishi Electric

Headquarters: Tokyo, Japan

Revenue: $36 billion+

Core rivalry: Automation, robotics, transportation systems

Competitive Edge: Strong Asian market dominance, Expertise in power electronics

Mitsubishi Electric is one of the most diversified industrial and electronics manufacturers, operating across automation, robotics, semiconductors, HVAC systems, transportation systems, satellites, and power equipment.

It is among the top global suppliers of Programmable Logic Controllers (PLCs), industrial robots, inverters, CNC systems, servo motors, and factory automation software. Its Factory Automation (FA) and Industrial Automation Systems are particularly dominant in Japan and Asia, where millions of production lines deploy its automation systems.

The competition between Mitsubishi and Siemens is especially strong in PLCs. Mitsubishi’s MELSEC PLCs directly compete with Siemens’ SIMATIC PLCs worldwide. Mitsubishi is often the preferred choice for high-speed manufacturing environments, such as electronics assembly and automotive parts production.

In infrastructure, Mitsubishi competes with Siemens Mobility across rail traction systems, signaling technologies, and power distribution equipment. In the energy sector, it rivals Siemens in transformers, switchgear, and smart grid systems.

Mitsubishi emphasizes innovation and R&D. For example, it ranked 4th globally for the number of international patent applications filed in 2023, according to the World Intellectual Property Organization (WIPO).

In FY 2025, Mitsubishi Electric reported about $36.8 billion in revenue and $42.56 billion in total assets, and employed around 149,914 people worldwide.

5. Rockwell Automation

Headquarters: Wisconsin, US

Revenue: $8.34 billion+

Core rivalry: PLCs, factory automation, industrial software

Competitive Edge: Dominant PLC market share in North America

Although Rockwell is significantly smaller than giants like Siemens, it has enormous strategic importance due to its laser-focused expertise in factory automation, control systems, industrial software, and smart manufacturing solutions.

Rockwell is widely known for its Allen-Bradley brand of PLCs, motor control systems, variable-frequency drives, and industrial sensors. These products form the operational backbone of thousands of factories worldwide. Plus, Rockwell’s ControlLogix and CompactLogix PLC families have become industry benchmarks for reliability and ease of integration.

The company has built a strong digital ecosystem through its FactoryTalk software platform, which integrates industrial automation with analytics, SCADA systems, Manufacturing Execution Systems (MES), and IIoT capabilities.

With the increase in adoption of smart factories and Industry 4.0 technologies, Rockwell aggressively expanded into cloud-based analytics, machine learning platforms, and cybersecurity (often through partnerships with Microsoft and Cisco).

In FY 2025, the company reported $3.52 billion in gross profit and $867 million in net income. Its R&D spending reached $679 million, a 3.19% increase from 2024. [11]

4. Philips Healthcare

Founded in 1891Headquarters: Amsterdam, Netherlands

Revenue: $20.2 billion+

Core rivalry: Medical imaging, diagnostic equipment

Competitive Edge: Ultrasound & patient monitoring systems

Philips has transformed from a light bulb manufacturer into a global health technology leader over the past several decades. Today, it generates approximately $20 billion in annual revenue (with healthcare accounting for nearly all of it).

The company’s mission is to improve people’s health and well-being through meaningful innovation. It has set a goal to improve 2.5 billion lives each year by 2030, including 400 million people in underserved communities.

Philips is widely known for its leadership in advanced ultrasound, cardiac monitoring, ICU technologies, CT scanners, MRI systems, and radiology workflow platforms. It is especially strong in patient monitoring systems, where it maintains one of the largest market shares globally. Their monitors and ICU systems are used across thousands of hospitals across Europe, North America, and Asia.

Philips invests about $2 billion each year in research and development. Its large intellectual property portfolio includes 50,500 patent rights, 30,500 trademarks, and 150,000 design rights. [12]

They emphasize streaming data, cloud/analytics, and remote monitoring solutions, reflecting the shift in healthcare toward remote/connected care. This gives it an edge over companies that are heavy on hardware only.

3. GE HealthCare

Headquarters: Chicago, Illinois, US

Revenue: $20.2 billion+

Core rivalry: MRI, CT, ultrasound, & diagnostic imaging

Competitive Edge: Strong US hospital penetration

GE HealthCare is one of the world’s most advanced medical technology and diagnostics companies, with a long history rooted in General Electric’s healthcare division dating back to the early 20th century.

The company focuses on medical imaging, diagnostic systems, ultrasound, patient monitoring solutions, and clinical software platforms. It is among the top three medical imaging companies globally, competing directly with Siemens Healthineers.

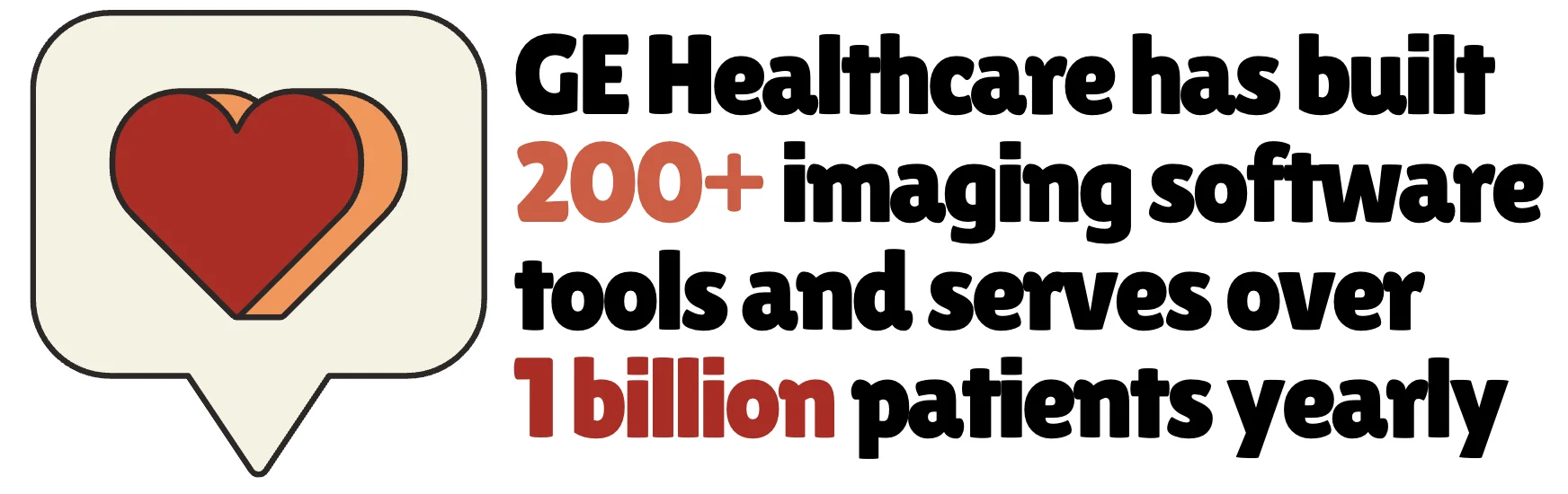

Its product portfolio includes MRI systems, CT scanners, X-ray devices, PET/CT machines, ultrasound systems, anesthesia monitors, ICU monitoring platforms, and advanced diagnostic software. The company has installed more than 5 million units worldwide, giving it one of the largest installed bases in the global medical technology sector.

While Siemens Healthineers is strong in data-heavy software for radiology and advanced imaging, GE HealthCare has invested heavily in AI-driven workflow optimization, cloud-linked imaging devices, and command center platforms for hospitals. Both companies also compete through integrated care pathways for oncology, cardiology, neurology, and emergency medicine. [13]

2. Schneider Electric

Founded in 1836Headquarters: Rueil-Malmaison, France

Revenue: $41 billion+

Core rivalry: Smart infrastructure, electrical distribution

Competitive Edge: Global leader in low-voltage equipment

Schneider Electric is best known for its dominance in low-voltage electrical equipment, building automation systems, industrial control technologies, and digital energy management platforms.

With a workforce of approximately 160,000 employees, Schneider operates a massive global supply chain and serves millions of customers, from small buildings and factories to data centers, utilities, heavy industries, and smart city projects.

The company has built a strong position in digital automation and Industrial IoT through its flagship platform EcoStruxure, which connects millions of devices across buildings, industrial plants, data centers, and infrastructure.

EcoStruxure enables real-time energy optimization, monitoring, predictive maintenance, and automation. This platform directly competes with Siemens’ Desigo CC and Smart Infrastructure suite.

The rivalry is equally intense in industrial automation. Schneider’s Modicon PLCs, SCADA systems, industrial drives, and automation hardware compete with Siemens’ SIMATIC PLCs, TIA Portal, SINAMICS drives, and distributed automation solutions.

In terms of innovation, Schneider invests over $1.4 billion annually in R&D, much of it focused on IoT, AI-driven automation, sustainability analytics, and cybersecurity. [14]

1. ABB Ltd

Founded in 1988Headquarters: Zurich, Switzerland

Revenue: $34.5 billion+

Core rivalry: Industrial automation, electrification, robotics

Competitive Edge: Breadth of portfolio + integrated solution

ABB’s mission is “to enable a more sustainable and resource-efficient future” by connecting engineering and digitalisation expertise.

Compared to Siemens, which leads in high-end industrial software, ABB counters with one of the largest robotics divisions and a much deeper focus on electrical components and power technologies.

ABB is a pioneer in electrical systems, having developed world-leading High Voltage Direct Current (HVDC) technology, which is essential for large-scale energy transmission. [15]

It is also one of the top three robotics companies globally, with its robotics division supplying industrial robots, autonomous systems, and AI-driven automation to automotive, electronics, consumer goods, and aerospace manufacturers worldwide.

The company has installed more than 500,000 robots worldwide, primarily in the automotive industry, and continues to expand its portfolio. It also has over 10,000 robots operating in the electronics sector and a dedicated factory for producing robots in the US.

What stands out is ABB’s recent pivot toward high-growth trends: electrification of infrastructure, smart buildings, digital industry, renewable energy integration, and electric mobility. For example, the company targets comparable revenue growth of 5-7 % through the economic cycle. The business model is increasingly oriented toward services and software overlays rather than purely hardware.

Read More

- 16 Best IFTTT Alternatives To Automate Your Online Workflow

- 16 Largest Chemical Companies In The World

- 5 Types Of Industries [With Examples]

- Press Release: Siemens is the European patent champion, Siemens

- Industry Analysis, Industrial automation and control systems market, Grand View Research

- Press Release: Omron exceeds 400M BPMs sold, Omron

- Financial Results: R&D expenses and Capex of the company, Yokogawa

- News and Events, Yokogawa recognized with double ‘A’ score, Yokogawa

- News, Danfoss enters deep electrification cooperation with major OEMs in China, Danfoss

- Financial Results, Emerson Electric 2025 full year revenue and net income, AInvest

- Financial Report, Main events of FY 2025, Alstom

- Business: Amprion, Hitachi Energy sign over $2 bln contract for German converter stations, Reuters

- Company Financials, Honeywell’s total assets throughout the years, Macrotrends

- Company Financials, Rockwell’s R&D expenses throughout the years, Macrotrends

- News, Philips tops European patent office Medtech filings in 2024, Philips

- Investor Relations, GE HealthCare invests in AI-enabled medical devices, GE HealthCare

- Financial Report, Record full-year results with accelerated execution in Q4, Schneider Electric

- News, ABB achieves breakthrough with world’s most powerful HVDC transformer, ABB