The history of hedge funds can be traced back to the bull market of the 1920s, when private partnership funds were backed and sustained by wealthy investors. After several ups and downs throughout the mid-20th century, the hedge fund industry was revived by the stock market boom of the 1990s.

Hedge funds make money by charging fees to their clients, typically a management fee and a performance fee. The industry average ranges from 2% to 20%.

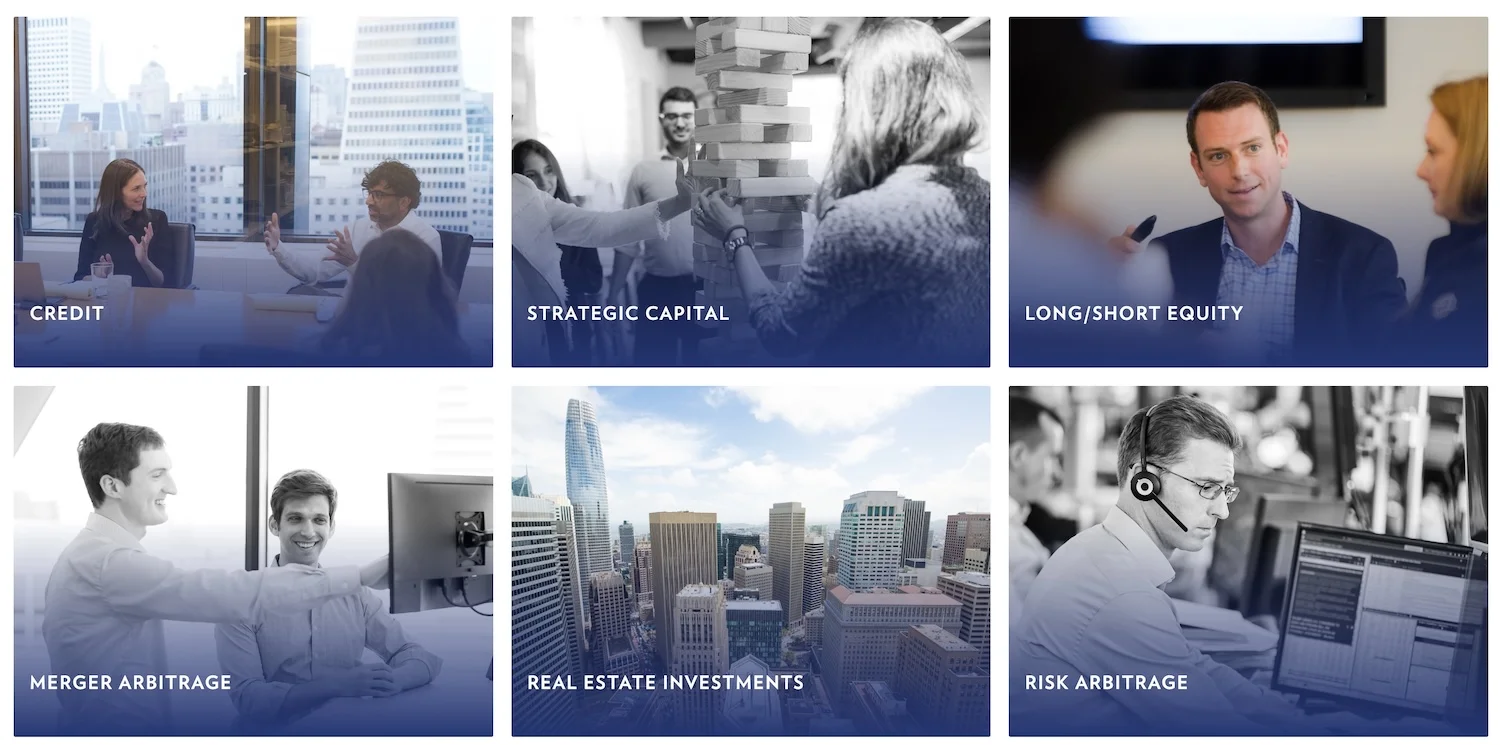

Apart from simply buying and selling equity, modern hedge funds have expanded to include credit and merger arbitrage, fixed income, quantitative strategies, multi-strategy approaches, distressed securities, and other investment strategies.

In 2008, the total assets managed by the entire hedge fund industry amounted to $2.2 trillion. Unfortunately, the financial crisis and credit crunch of that year significantly reduced their assets under management (AUM), and it took nearly eight years for the industry to recover.

By the end of 2017, the industry reported a record with $2.9 trillion in AUM. Moving ahead to 2025, the global assets managed by hedge funds soared to $4.74 trillion.

Below, we have highlighted some of the world’s largest hedge funds, considering factors such as their Assets Under Management (AUM), historical performance, and reputation and influence in the finance industry.

Did you know?

The Medallion Fund, created in 1988 and overseen by Renaissance Technologies, stands out as a highly successful investment fund. It has generated tens of billions of dollars in returns since its inception, maintaining an average annual return of 66% before fees and approximately 39% after fees from 1988 to 2018.

Table of Contents

14. AQR Capital Management

Founders: Cliff Asness and three others in 1998

AUM: $160.5 billion

Competitive Edge: Deep research and academic foundations

AQR Capital Management is one of the largest quantitative hedge funds in the world that provides both traditional and alternative investment opportunities for investors.

The firm puts a strong emphasis on portfolio diversification and is known to utilize multiple investment styles — value, defensive, carry, and momentum investing.

AQR played a crucial role in enhancing the marketability of alternative mutual funds following the 2008 global financial crisis. It is primarily controlled by its three billionaire founders, Cliff Asness, David Kabiller, and John Liew, as well as other principal members.

Cliff Asness has admitted that AQR is now “surrendering more to the machines,” meaning it is relying more on AI and machine-learning models when making investment decisions.

13. Baupost Group

Seth Klarman

Seth Klarman

Founders: Seth Klarman and William Poorvu in 1982

AUM: $23.6 billion

Competitive Edge: Conservatism & discipline, Contrarian insight

The Baupost Group was founded in 1982 by four partners: William Poorvu, Jordan Baruch, Howard Stevenson, and Issac Auerbach. They were later joined by Seth Klarman, who currently heads the firm and serves as its president. As a value investor, Klarman is often dubbed the “next Warren Buffett.”

Based in Boston, the Baupost Group is recognized for its risk management practices, and under Seth Klarman’s leadership, it has become the world’s largest hedge fund to adhere to value investing norms.

Unlike many large hedge funds and asset management firms, Baupost does not take advantage of leverage (borrowed money) while investing in most asset classes, with the exception of real estate.

In recent years, the Group has focused more on managing downside risk and preserving capital. It now makes sure that every position not only has a good valuation but also a clear path or catalyst for gains. It also puts more thought into what to sell (not just what to buy) when funding new investments.

12. Marshall Wace

Founders: Paul Marshall and Ian Wace in 1997

AUM: $88.78 billion

Competitive Edge: Blended strategy and flexibility

Marshall Wace is a London-based hedge fund with over 25 years of experience in the industry. It was established by Paul Marshall, who previously worked at the biggest investment management firm in Britain, and Ian Wace, who served as the head of equity trading in the Deutsche Bank investment arm with about the $50 million of seed money.

Marshall Wace practices several investment techniques and strategies and is reasonably flexible on how it commits its investors’ capital. The firm specializes in a long-short strategy.

In 2015, private equity giant Kohlberg Kravis Roberts bought a 24.6 percent stake in Marshall Wace, which was increased to 39 percent in November 2019. After the stake acquisition, both firms entered into a strategic partnership focused on co-developing new investment products and strategies.

In 2023, the firm generated $1.52 billion in revenue, a decrease from the $1.9 billion reported in the previous year. The profits, which stood at $683 million, were distributed among 26 partners.

In 2025, the firm reported $88.8 billion in total securities holdings in its SEC filing.

11. Davidson Kempner Capital Management

Headed by: Anthony A. Yoseloff (Executive Managing Member)

AUM: $43.5 billion

Competitive Edge: Expertise in distressed assets, strong downside protection

Davidson Kempner Capital Management was initially named M.H. Davidson & Co. when Marvin H. Davidson founded it in 1983. The firm was renamed when Thomas L. Kempner, Jr, joined the firm in 1984. He was appointed as Executive Managing Member in 2004.

This New York City-based hedge fund relies on a bottom-up analysis of the market to make investment decisions with a prime focus on distressed securities, merger arbitrage, long/short equity, credit, and convertible bonds arbitrage strategy.

In 2024, Davidson Kempner closed its Distressed Opportunities Fund, which had about $2 billion under management, because the returns were seen as too low for the current market environment. At the time it was closed, the fund had delivered roughly a 5% return year-to-date.

However, the firm will continue investing in distressed assets through its closed-end funds and multi-strategy funds, rather than through that specific dedicated fund.

10. Citadel

Founder: Kenneth C. Griffin

AUM: $67 billion

Competitive Edge: Combination of scale + infrastructure + talent

The founder and CEO of Citadel LLC established the company in 1990 with the financial backing of his former employer and mentor, Frank Mayer. After a couple of tough years, the firm witnessed a meteoric rise in annual AUM, as well as, in popularity.

But everything changed in late 2008 when the financial crisis hit the hedge fund head-on, just like any other financial company at that time. However, the excessive and unexpected loss in the financial meltdown led the firm to focus on risk management more than ever before.

Citadel has a dedicated risk management center that enables the firm not only to monitor its assets and investments closely but also to conduct numerous stress tests to anticipate and avert any potential crisis. The firm’s excessive focus on risk management has played a key role in its success after the 2008 crisis so far.

In a bond prospectus, Citadel reported that from 2021 to September 2024, its largest multistrategy funds (Wellington, Kensington, and Kensington II) generated about $56.8 billion in gross gains. After fees, performance charges, and pass-through costs, investors earned roughly $30 billion in net gains.

The firm also disclosed about $7.5 billion in management and performance fees, along with about $17 billion in pass-through expenses, nearly 90% of which went toward employee compensation.

9. Farallon Capital

Founder: Tom Steyer in 1986

AUM: $42 billion

Competitive Edge: Deep senior investment team with long average tenure

Farallon Capital was established in 1986 by Tom Steyer, who previously worked at investment management and financial services firms, including Hellman & Friedman, Goldman Sachs, and Morgan Stanley. In the PE firm Hellman & Friedman, Steyer worked as a risk arbitrage trader, a complex investment strategy that he would later use in his hedge fund.

The firm makes use of various investment strategies to generate profits for its clients. One of those strategies is merger (risk) arbitrage, a type of event-driven investing in which investors take advantage of pricing inefficiencies caused by a major event in a company.

Farallon Capital is also a pioneer of university endowments in the United States. In 1987, a year after establishing his firm, Tom Steyer went back to Yale to pursue the university’s endowment as a client. Initially, Farallon managed Yale’s endowment fund without fees, but that changed after it became a success.

These days, Farallon is taking an aggressive approach to shareholder activism, particularly in Japan. The companies it targets (such as Astellas and T&D) are large and have areas that Farallon believes are underperforming.

8. Two Sigma Investments

Founder: John Overdeck, David Siegel, and Mark Pickard

AUM: $110.3 billion

Competitive Edge: Scientific culture + research orientation

Founded in 2001, Two Sigma is the youngest hedge fund on this list. But despite its relatively low experience, the company has managed to outperform other, much older hedge funds through its automated investment/trading strategies, which involve the use of AI and machine learning.

In 2014, Two Sigma raised about $3.3 billion for their new macro fund, which happens to be the largest of a kind capital raised since the 2008 crisis. The firm, much like tech companies, employs various crowd-sourcing options to develop trading algorithms.

Its unusual name, “Two Sigma,” reflects the dichotomy of the mathematical word sigma in which the lower case sigma, σ, represents the volatility in investment returns, while the upper case sigma, Σ, denotes the sum.

In recent years, the company has gone through leadership changes. These transitions may shift priorities in areas like risk management, resource allocation, and the balance between research and model safety. The fact that internal disagreements became public also points to a growing push for greater stability.

7. D.E. Shaw & Co.

Founder: David E. Shaw in 1988

AUM: $70 billion

Competitive Edge: Risk discipline and long-term thinking

D.E. Shaw is one of the most successful and respected investment management firms globally. It is widely recognized for its quantitative investment approach, which utilizes complex mathematical and statistical models to inform investment decisions. However, the firm also makes its investment decisions based on fundamental analysis and human judgment.

Since its early days, D.E. Shaw has focused on recruiting talented mathematicians, programmers, and scientists to develop its own trading algorithms and scientific research.

Two of its former employees, David Siegel and John Overdeck, went on to establish their own hedge fund, Two Sigma Investments, in 2001. Jeff Bezos, who later founded the Amazon empire, also contributed his expertise during a four-year tenure at D.E. Shaw.

In 2018, Institutional Investor magazine ranked D.E. Shaw & Co. as the fifth-highest hedge fund earner of all time. It was named Hedge Fund of the Year for multi-strategy long-term performance and macro (exceeding $10 billion) by HFM, a market intelligence firm specializing in hedge funds, in 2020.

In 2025, D. E. Shaw bought a stake in Riot Platforms, a bitcoin mining company. Sources suggest it may push for changes, such as making better use of the firm’s power capacity, potentially for AI or high-performance computing.

6. The Children’s Investment Management Fund (TCI)

Founder: Chris Hohn in 2003

AUM: $70 billion

Competitive Edge: High conviction, concentrated bets

The Children’s Investment Management Fund may not sound like a hedge fund at all. However, with about $70 billion in assets under management, it is surely one of the largest hedge funds in the world.

The firm derives its name from an international charitable foundation known as The Children’s Investment Fund Foundation or CIFF, which focuses on improving children’s lives globally. In the investment world, the firm is more popularly known as TCI Fund Management or simply TCI.

Like other large hedge funds, TCI engages in long-term investments. It is widely known as an activist hedge fund that frequently acquires a modest ownership stake in a company to encourage its management to meet corporate objectives. One of the best examples of TCI’s successful activist campaign is the split-up of the original ABN AMRO, a Dutch bank, in 2007.

TCI faced heavy losses during the 2008 financial crisis. At that time, its AUM stood at about $6 billion. In 2010, the firm recorded an 80 percent loss in profits. However, TCI made huge gains in the following decade with successful investments in relatively risky companies, such as News Corp. and Japan Tobacco.

As of 2025, TCI’s 13F portfolio held about $50.7 billion in equities across only 10 stocks. With such a concentrated portfolio, the firm faces significant idiosyncratic risk.

5. Elliott Management Corporation

Paul Singer

Paul Singer

Founder: Paul Singer

AUM: $76.1 billion

Known For: Investing in distressed securities

Elliot Management Corporation is a New York-based hedge fund specializing in currencies, commodities, equities, and other asset classes. It’s also known for investing in distressed securities, including sovereign or government debt.

The founder and co-CEO of Elliot Management, Paul Singer, is a respected and perhaps one of the most feared money managers in the world. His bold investment strategies, such as shareholder activism and investing in near-bankrupt companies, have earned him the tag of a “vulture capitalist.”

Paul Singer and his firm get attention from the media on an international stage from time to time. One such incident was in 2002 over Argentina’s sovereign debt default. Then, in 2007, Elliot Associates coincidentally exposed corruption in the Republic of the Congo while trying to recover its default bank debt.

In 2025, Elliott made several major investments: a $4 billion stake in PepsiCo, more than $2.5 billion in Phillips 66, over $5 billion in Honeywell, nearly a 5% stake in BP, more than $1.5 billion in HPE, and over $2 billion in Workday.

4. Millennium Management

Founder: Israel Englander

AUM: $79 billion

Competitive Edge: Diversification of strategy/risk

Millennium Management, established by U.S.-born investor Israel Englander in 1989 with a modest seed capital of just over $2 million, has grown into one of the world’s largest hedge funds. Despite a challenging beginning, the firm experienced a swift ascent to prominence.

Over the years, Millennium Management has mastered various investment strategies like convertible arbitrage, in which investors take advantage of the price difference between the company’s share price and the convertible bond, and merger arbitrage, which involves buying and selling stocks of two merging companies.

Millennium’s multi-team, multi-strategy model offers flexibility, but it also means each pod is exposed to very different risks. Some teams are performing well, while others are under pressure, especially those using more crowded, leveraged, or volatile strategies.

According to Institutional Investor magazine, Israel Englander was the fifth-highest-earning hedge fund manager, bagging $975 million in 2017.

In 2020, the firm oversaw more than 2,000 data sets sourced from 400 providers, comprising nearly 10 trillion data records and 2,000 terabytes of compressed stored data.

In 2024, its flagship fund reportedly returned about 15.1%. However, in FY 2025, two of Millennium’s teams that focus on index-rebalancing strategies suffered significant losses, estimated at around $900 million in total.

3. Renaissance Technologies

Jim Simons

Jim Simons

Founder: James Harris Simons

AUM: $92 billion

Competitive Edge: Speed + precision in quant model building

Renaissance Technologies is another New York-based quantitative hedge fund that was founded in 1982 by James Harris Simons, a renowned mathematician who also served as a code breaker during the Cold War.

The firm excels in the systematic trading environment, focusing on ingeniously developed quantitative models or investment algorithms.

It is one of the earliest proponents of quantitative trading, a specialized field in which researchers analyze decades of financial data and extract valuable information in order to predict various economic and financial market trends.

The Medallion fund, Renaissance’s flagship offering, has generated annualized returns of about 37% after fees since its launch in 1988. However, the fund is available only to company employees.

There is a noticeable performance gap between RenTech’s different funds, both internal and external. Some are still generating positive returns, while others are not. This suggests that the external funds (or those with greater exposure to equity and macro trends) may be more vulnerable.

2. Bridgewater Associates

Ray Dalio

Ray Dalio

Founder: Ray Dalio in 1975

AUM: $136.5 billion

Known For: Risk Parity, Daily Observations

One of the world’s largest hedge funds, Bridgewater Associates, was founded in 1975 by Ray Dalio in his Manhattan-based apartment. The firm acted as an advisory service during its early years, providing exclusive economic insights to various institutional clients, including McDonald’s.

Throughout the 1980s and 90s, the firm established new benchmarks in specialized areas like global bonds, inflation-indexed bonds, and currency overlay. Bridgewater also pioneered multiple unconventional investment strategies known as Pure Alpha and All-Weather funds.

Specializing in the global macro strategy, the firm makes strategic decisions by considering factors such as currency exchange rates, gross GDP, inflation, and other relevant economic indicators.

In 2018, Bridgewater Associates surpassed the S&P 500, other major benchmark indices, and many of its competitors. Moving to 2021, the firm delivered a significant 7.8% return, representing its most robust annual performance since 2018.

However, in 2023, the flagship hedge fund of Bridgewater Associates experienced a setback, losing 7.6%, with the entire decline occurring in the last two months of the year. In July 2025, Ray Dalio sold his remaining ownership stake in the firm.

In 2025, Bridgewater sold its stakes in several US-listed Chinese companies, including Alibaba, Baidu, JD.com, PDD Holdings, and Yum China. At the same time, the firm increased positions in major US tech companies such as Microsoft and Nvidia and added new stakes in ARM Holdings.

It also reduced or exited less favorable holdings, like cutting back exposure to Apple, while rotating into sectors it views as offering higher growth or better risk/reward opportunities.

1. Man Group

Founder: James Man in 1783

AUM: $193.3 billion

Competitive Edge: Scale, diversification, and strong client inflows

Man Group plc, a British multinational investment management firm, is currently the world’s largest publicly traded hedge fund company. Founded in 1783 as a sugar brokerage, the firm expanded its trade to include other commodities like cocoa and coffee. By the end of the 19th century, it had further diversified into a range of financial services and products.

Today, the group is composed of five divisions – Man AHL, Man Numeric, Man GLG, Man FRM, and Man GPM – all focusing on different investment approaches and strategies. Most of these divisions have been created over time through acquisitions.

Apart from investing, Man Group sponsors a private charitable trust that supports education for disadvantaged individuals. Until 2019, it sponsored Britain’s most coveted literary prize, the Booker Prize.

In mid 2025, , Man Group reported a record AUM of $193.3 billion, up from $168.6B at end-2024. Net inflows over the first half of 2025 were about $17.6 billion. Most of this growth came from long-only strategies, especially systematic and quant-driven approaches, rather than alternative or hedge fund products.

Read: 20 Most Successful Investors In The World

How do hedge funds make money?

Hedge funds pool money from investors and invest that capital in different asset classes across the market with the intention of generating returns. Historically, hedge funds tend to invest more in public markets than private equity and use complex techniques such as short selling, arbitrage, and derivatives.

Hedge funds make money in two ways: Management fees and Performance fees. A management fee is a recurring fee levied by a hedge fund manager to cover operating expenses. It is typically 2% of the fund’s AUM or asset under management.

In addition to management fees, hedge funds also charge performance fees. It is the percentage of profits from investments, usually 20%. While the exact fee structure varies from fund to fund, most of them follow the 2 and 20 rules.

Why is it called a ‘hedge fund’?

In finance, hedging is an investment strategy that enables investors to mitigate exposure to risk associated with their investments, thereby making them more secure during market fluctuations.

Today, hedge funds utilize various complex financial instruments to protect their investments, including forward and futures contracts, swaps, and options.

However, hedge funds got their name from early fund managers who specialized in a single hedging strategy known as the long/short equity model, in which a trader tries to mitigate investment risk by short-selling.

Do hedge funds ever lose money?

The primary objective of hedge funds is to generate a profit regardless of market conditions. Losses and failure are simply unacceptable. However, hedge funds do lose money, incur heavy losses, and, in extreme cases, are forced to shut down.

Due to the competitive nature of the business, the investment strategies employed by hedge funds are typically high-risk. One of the biggest factors that can lead to hedge fund failure is high leverage. Perhaps the most famous and well-documented hedge fund failure is the collapse of Long-Term Capital Management (LTCM).

LTCM was established in 1994, focusing on arbitrage strategies that take advantage of pricing differences in two or more markets. In its second year alone, the hedge fund made annualized returns of 43 percent (after fees). However, exposure to the 1998 Russian Financial crisis, primarily through derivatives and high leverage, ultimately resulted in its collapse.

Can anyone start a hedge fund?

The underlying risks, legal aspects, and capital requirements of hedge funds make them completely different from ordinary businesses. Typically, hedge funds are started by highly experienced investment managers skilled in complex investment strategies.

According to a report by Grant Thornton, one of the largest accounting firms in the United States, establishing a hedge fund startup in the US costs anywhere between $50,000 and $150,000. A crucial aspect of starting a hedge fund is legal compliance, which requires the right kind of attorney.

The bottom line is that starting a hedge fund requires significantly more money than an ordinary business, advanced investment skills, and some luck.

Read More

To tell the truth, before this moment I hadn’t been really aware of Hedge Funds, but it has been really interesting for me to delve into this concept and understand how they operate. It is so interesting that Hedge Funds include so many investment strategies which make them truly unique. I know that such funds have different types and I can say that all these mentioned largest hedge funds in the world have their own special distinctive features and I really like the fact that they all provide investors with a great deal of opportunities that unites these funds, standing out from others. I really like the strategy of Baupost Group and their business practices because they act in a really wise and smart way, having really interesting concepts.